ACGL (Property & Casualty Insurance) discloses SEC-backed natural gas exposure: "oil, natural gas); (ii) advances in low-carbon technology and renewable energy development; and (iii) effects of extreme weather events on t"; the impact can be mixed or context-dependent.

Connection details

oil, natural gas); (ii) advances in low-carbon technology and renewable energy development; and (iii) effects of extreme weather events on the physical and operational exposure of industries and issuers, and the transition that these companies make towards addressing climate risk in their own businesses

ACGL (Property & Casualty Insurance) discloses SEC-backed foreign exchange exposure: "Total return is calculated on a pre-tax basis before investment expenses and reflects the effect of financial market conditions along with f"; the impact can be mixed or context-dependent.

Connection details

Total return is calculated on a pre-tax basis before investment expenses and reflects the effect of financial market conditions along with foreign currency fluctuations

ACGL (Property & Casualty Insurance) discloses SEC-backed tariffs exposure: "This risk may be heightened from time to time by geopolitical tensions, global supply chain disruptions, tariffs, and other contributing fac"; the impact can be mixed or context-dependent.

Connection details

This risk may be heightened from time to time by geopolitical tensions, global supply chain disruptions, tariffs, and other contributing factors

ACGL (Property & Casualty Insurance): included because this issuer's sector is structurally sensitive to rates, funding costs, credit, or capital allocation.

ACGL (Property & Casualty Insurance): included because weather and hurricane outcomes can affect claims, power reliability, travel, facilities, or regional operations.

Connection details

4%

96% NO

24H 3–4%

Bid 3¢

Ask 4¢

Spread 1.0 pts

$1.6K 24H

$2.7K total

$2.6K OI

Open

Closes Dec 1

80%

accepted

Operating risk graph

Filing-backed exposures

Kosmos extracts named operating factors from supported company filings. Expand a factor to inspect every returned receipt and its original source.

97

Factors

17

Mixed

91

Directional

6

Inflation Expectations14 filing receipts68% confidence86% max materialitymixed

In addition, governmental actions in response to inflationary pressures, such as increasing interest rates, may have a material impact, such as on the market value of our investment portfolio, or on the size of the mortgage origination market available to be insured by our mortgage business

or loss of investments accounted for using the equity method, other income or loss, corporate expenses, transaction costs and other, amortization of intangible assets, interest expense, net foreign exchange gains or losses, income taxes, income from operating affiliates and items related to our non-cumulative preferred shares. Net Investment Income. The components of net investment income were derived from the following sources: Year Ended December 31, 2025 2024 Fixed maturities $ 1,465 $ 1,266 Short-term inv

or loss of investments accounted for using the equity method, other income or loss, corporate expenses, transaction costs and other, amortization of intangible assets, interest expense, net foreign exchange gains or losses, income taxes, income from operating affiliates and items related to our non-cumulative preferred shares. Net Investment Income. The components of net investment income were derived from the following sources: Three Months Ended March 31, 2026 2025 Fixed maturities $ 384 $ 342 Short-term in

• The effects of inflation, trade and tariff disputes and other economic conditions impact the insurance and reinsurance industry in ways which may negatively impact our business, financial condition and results of operations

are influenced by factors such as the frequency and/or severity of claims and losses, including natural disasters or other catastrophic events, variations in interest rates and financial markets, changes in the legal, regulatory and judicial environments, inflationary pressures and general economic conditions

natural disasters or other catastrophic events, variations in interest rates and financial markets, changes in the legal, regulatory and judicial environments, inflationary pressures and general economic conditions

Borrowers default for a variety of reasons, including a reduction of income, unemployment, divorce, illness, inability to manage credit, rising interest rate levels and declining home prices

In addition to the nature of property business, we believe that economic and geographic trends affecting insured property, including inflation, property value appreciation and geographic concentration, tend to generally increase the size of losses from catastrophic events over time

In addition, governmental actions in response to inflationary pressures, such as increasing interest rates, may have a material impact, such as on the market value of our investment portfolio, or on the size of the mortgage origination market available to be insured by our mortgage business

Borrowers default for a variety of reasons, including a reduction of income, unemployment, divorce, illness, inability to manage credit, rising interest rate levels and declining home prices

are influenced by factors such as the frequency and/or severity of claims and losses, including natural disasters or other catastrophic events, variations in interest rates and financial markets, changes in the legal, regulatory and judicial environments, inflationary pressures and general economic conditions

• The effects of inflation, trade and tariff disputes and other economic conditions impact the insurance and reinsurance industry in ways which may negatively impact our business, financial condition and results of operations

• The effects of inflation, trade and tariff disputes and other economic conditions impact the insurance and reinsurance industry in ways which may negatively impact our business, financial condition and results of operations

Company Kpi8 filing receipts63% confidence78% max materialitymixed

Company Kpi

Company operating metrics

Company Kpi63% confidence

expense ratio 20.0 % 18.5 % 1.5 Other operating expense ratio (2) 16.3 % 15.6 % 0.7 Combined ratio 96.5 % 100.1 % (3.6) (1) ‘Other underwriting income’ includes revenue earned from underwriting-related activities covered under existing service contracts. (2) The ‘Other operating expense ratio’ includes ‘Other underwriting income.’ See ‘Comments on Non-GAAP Financial Measures’ for further details. ARCH CAPITAL 40 2026 FIRST QUARTER FORM 10-Q Table of Contents Premiums Written . The following

to provide internal reinsurance covering certain U.S. lines of business. AGRL is a U.S. taxpayer through a section 953(d) voluntary election under the Internal Revenue Code of 1986, as amended. Strategy. Our reinsurance group’s strategy is to capitalize on our financial capacity, experienced management and operational flexibility to offer multiple products through our operations. The reinsurance group’s operating principles are to: • Actively select and manage risks . Our reinsurance group only

expense ratio 19.3 % 18.4 % 0.9 Other operating expense ratio (2) 14.6 % 15.0 % (0.4) Combined ratio 95.2 % 94.8 % 0.4 (1) ‘Other underwriting income’ includes revenue earned from underwriting related activities covered under existing service contracts. (2) The ‘Other operating expense ratio’ for the 2025 period includes ‘Other underwriting income.’ See ‘Comments on Non-GAAP Financial Measures’ for further details. ARCH CAPITAL 75 2025 FORM 10-K The insurance segment consists of our insura

policies, practices or regulations change, the amount of mortgage insurance we write in the U.S. or Australia could decline, which would reduce our mortgage insurance revenues. • Changes to the role of the GSEs in the U.S. housing market or to GSE eligibility requirements for mortgage insurers or to the GSEs’ use of CRT could negatively impact our results of operations and financial condition or reduce our operating flexibility. • The implementation of the Basel III Capital Accord and FHFA’s Enterpri

expense ratio 19.3 % 18.4 % 0.9 Other operating expense ratio (2) 14.6 % 15.0 % (0.4) Combined ratio 95.2 % 94.8 % 0.4 (1) ‘Other underwriting income’ includes revenue earned from underwriting related activities covered under existing service contracts. (2) The ‘Other operating expense ratio’ for the 2025 period includes ‘Other underwriting income.’ See ‘Comments on Non-GAAP Financial Measures’ for further details. ARCH CAPITAL 75 2025 FORM 10-K The insurance segment consists of our insura

policies, practices or regulations change, the amount of mortgage insurance we write in the U.S. or Australia could decline, which would reduce our mortgage insurance revenues. • Changes to the role of the GSEs in the U.S. housing market or to GSE eligibility requirements for mortgage insurers or to the GSEs’ use of CRT could negatively impact our results of operations and financial condition or reduce our operating flexibility. • The implementation of the Basel III Capital Accord and FHFA’s Enterpri

to provide internal reinsurance covering certain U.S. lines of business. AGRL is a U.S. taxpayer through a section 953(d) voluntary election under the Internal Revenue Code of 1986, as amended. Strategy. Our reinsurance group’s strategy is to capitalize on our financial capacity, experienced management and operational flexibility to offer multiple products through our operations. The reinsurance group’s operating principles are to: • Actively select and manage risks . Our reinsurance group only

expense ratio 20.0 % 18.5 % 1.5 Other operating expense ratio (2) 16.3 % 15.6 % 0.7 Combined ratio 96.5 % 100.1 % (3.6) (1) ‘Other underwriting income’ includes revenue earned from underwriting-related activities covered under existing service contracts. (2) The ‘Other operating expense ratio’ includes ‘Other underwriting income.’ See ‘Comments on Non-GAAP Financial Measures’ for further details. ARCH CAPITAL 40 2026 FIRST QUARTER FORM 10-Q Table of Contents Premiums Written . The following

Housing Demand8 filing receipts72% confidence78% max materialitymixed

HousingMortgage RatesFed Rates

Housing demand

Housing Demand76% confidence

ultimate performance of our mortgage insurance portfolios remains uncertain. • If the volume of low down payment mortgage originations declines, or if other government housing policies, practices or regulations change, the amount of mortgage insurance we write in the U.S. or Australia could decline, which would reduce our mortgage insurance revenues. • Changes to the role of the GSEs in the U.S. housing market or to GSE eligibility requirements for mortgage insurers or to the GSEs’ use of CRT could negati

insurance and reinsurance to the Australian market. Strategy . The mortgage insurance market operates on a distinct underwriting cycle, with demand driven mainly by the housing market and general economic conditions. As a result, the creation of the mortgage group provides us with a more diverse revenue stream. Our mortgage group’s strategy is to capitalize on its financial capacity, mortgage insurance technology platform, operational flexibility and experienced management to offer mortgage insurance, reinsu

a proprietary risk model (“Realistic Disaster Scenario” or “RDS”) that simulates the maximum loss resulting from a severe economic downturn impacting the housing market. The RDS models the collective impact of adverse conditions for key economic indicators, the most significant of which is a decline in home prices. The RDS model projects paths of future home prices, unemployment rates, income levels and interest rates and assumes correlation across states and geographic regions. The resulting fu

a proprietary risk model (“Realistic Disaster Scenario” or “RDS”) that simulates the maximum loss resulting from a severe economic downturn impacting the housing market. The RDS models the collective impact of adverse conditions for key economic indicators, the most significant of which is a decline in home prices. The RDS model projects paths of future home prices, unemployment rates, income levels and interest rates and assumes correlation across states and geographic regions. The resulting fu

insurance and reinsurance to the Australian market. Strategy . The mortgage insurance market operates on a distinct underwriting cycle, with demand driven mainly by the housing market and general economic conditions. As a result, the creation of the mortgage group provides us with a more diverse revenue stream. Our mortgage group’s strategy is to capitalize on its financial capacity, mortgage insurance technology platform, operational flexibility and experienced management to offer mortgage insurance, reinsu

a proprietary risk model (“Realistic Disaster Scenario” or “RDS”) that simulates the maximum loss resulting from a severe economic downturn impacting the housing market. The RDS models the collective impact of adverse conditions for key economic indicators, the most significant of which is a decline in home prices. The RDS model projects paths of future home prices, unemployment rates, income levels and interest rates and assumes correlation across states and geographic regions. The resulting fu

ultimate performance of our mortgage insurance portfolios remains uncertain. • If the volume of low down payment mortgage originations declines, or if other government housing policies, practices or regulations change, the amount of mortgage insurance we write in the U.S. or Australia could decline, which would reduce our mortgage insurance revenues. • Changes to the role of the GSEs in the U.S. housing market or to GSE eligibility requirements for mortgage insurers or to the GSEs’ use of CRT could negati

a proprietary risk model (“Realistic Disaster Scenario” or “RDS”) that simulates the maximum loss resulting from a severe economic downturn impacting the housing market. The RDS models the collective impact of adverse conditions for key economic indicators, the most significant of which is a decline in home prices. The RDS model projects paths of future home prices, unemployment rates, income levels and interest rates and assumes correlation across states and geographic regions. The resulting fu

Regulation8 filing receipts71% confidence78% max materialitymixed

Regulation

Regulation and enforcement

Regulation75% confidence

operating income available to Arch common shareholders and annualized operating return on average common equity are non-GAAP financial measures as defined in Regulation G

After-tax operating income available to Arch common shareholders, a non-GAAP financial measure as defined in Regulation G, represents net income available to Arch common shareholders, excluding net realized gains or losses (which include, but are not limited to, realized and unrealized changes in the fair value of equity securities and assets accounted for using the

(“Arch LMI”) was authorized by the Australian Prudential Regulation Authority (“APRA”) to write lenders’ mortgage insurance (“LMI”) on a direct basis in Australia

(“Arch LMI”) was authorized by the Australian Prudential Regulation Authority (“APRA”) to write lenders’ mortgage insurance (“LMI”) on a direct basis in Australia

operating income available to Arch common shareholders and annualized operating return on average common equity are non-GAAP financial measures as defined in Regulation G

After-tax operating income available to Arch common shareholders, a non-GAAP financial measure as defined in Regulation G, represents net income available to Arch common shareholders, excluding net realized gains or losses (which include, but are not limited to, realized and unrealized changes in the fair value of equity securities and assets accounted for using the

Foreign Exchange6 filing receipts81% confidence78% max materialitymixed

FxForeign Currency

Foreign exchange

Foreign Exchange86% confidence

Total return is calculated on a pre-tax basis and before investment expenses and reflects the effect of financial market conditions along with foreign currency fluctuations

Total return is calculated on a pre-tax basis before investment expenses and reflects the effect of financial market conditions along with foreign currency fluctuations

Total return is calculated on a pre-tax basis and before investment expenses and reflects the effect of financial market conditions along with foreign currency fluctuations

Total return is calculated on a pre-tax basis before investment expenses and reflects the effect of financial market conditions along with foreign currency fluctuations

Moreover, the intellectual property and ownership rights associated with both forms of artificial intelligence have not been fully addressed by courts in the U

Moreover, the intellectual property and ownership rights associated with both forms of artificial intelligence have not been fully addressed by courts in the U

Consumer Credit4 filing receipts80% confidence78% max materialitymixed

CreditDelinquencies

Consumer credit quality

Credit Quality84% confidence

of equity securities and assets accounted for using the fair value option, realized and unrealized gains or losses on derivative instruments, changes in the allowance for credit losses on financial assets and gains or losses realized from the acquisition or disposition of subsidiaries), equity in net income or loss of investments accounted for using the equity method, net foreign exchange gains or losses, transaction costs and other and income taxes. Management uses Operating ROAE as a key measure of the return

of equity securities and assets accounted for using the fair value option, realized and unrealized gains or losses on derivative instruments, changes in the allowance for credit losses on financial assets and gains or losses realized from the acquisition or disposition of subsidiaries), equity in net income or loss of investments accounted for using the equity method, net foreign exchange gains or losses, transaction costs and other, loss on redemption of preferred shares and income taxes. Management uses Operat

results of operation. • Foreign currency exchange rate fluctuation may adversely affect our financial results. • The determination of the amount of current expected credit losses (“CECL”) allowances taken on our investments is highly subjective and could materially impact our results of operations or financial position. • Our reinsurance subsidiaries may be required to provide collateral to ceding companies, by applicable regulators, their contracts or other commercial considerations. Their ability t

Our mortgage group has ceded a portion of its premium through quota share and aggregate excess of loss reinsurance agreements which provide reinsurance coverage for delinquencies on portfolios of in-force policies issued between certain periods. See note 8, “Reinsurance,” to our consolidated financial statements in Item 8 for further details. Reinsurance arrangements do not relieve our mortgage group from its primary obligations to insured parties. Reinsurance recoverables are recorded as assets, predi

Political Policy4 filing receipts69% confidence60% max materialitymixed

ElectionsPolicy

Elections and political policy

Election Policy69% confidence

• The impact of climate change will affect our loss limitation methods, such as the purchase of third party reinsurance and catastrophe risk modeling and risk selection in ways which may adversely impact our business, financial condition and results of operations. • Our insurance, reinsurance and mortgage subsidiaries are subject to supervision and regulation. Changes to existing regulation and supervisory standards, or failure to comply with applicable requirements, could adversely affect our busin

on average common equity of 17.8% and 15.4%, respectively. See “ Comment on Non-GAAP Financial Measures .” Critical to our cycle management is emphasizing risk selection, as we continue to leverage our diversified specialty platform and the expertise of our underwriting teams. We invest and use data and analytics to sharpen insights, enhance risk selection and deliver a differentiated customer experience while fostering a culture that attracts the best-in-class talent. We believe our balance sheet is i

property and casualty businesses, our commitment to deliver long-term value for our shareholders remains unchanged. Critical to our cycle management is emphasizing risk selection, as we continue to leverage our diversified specialty platform and the expertise of our underwriting teams. We invest and use data and analytics to sharpen insights, enhance risk selection and deliver a differentiated customer experience while fostering a culture that attracts the best-in-class talent. We closed 2025 with a balance she

our experience and strategic analytics to drive decisions . Our insurance group’s underwriting philosophy is to generate an underwriting profit through prudent risk selection and proper pricing. Our insurance group believes that the key to this approach is adherence to uniform underwriting standards across all types of business. Our insurance group’s senior management closely monitors the underwriting process. This strategy is underpinned by our belief in using data and strategic analytics to assess busin

Cybersecurity2 filing receipts74% confidence54% max materialitynegative

CybersecurityData Breach

Cybersecurity and data breach

Cybersecurity Risk74% confidence

• We could be materially impacted by a cyber attack, data breach, ransomware, phishing, social engineering or other cybersecurity incident resulting in loss of business data, personal data and other confidential or secret information, a disruption in our business operations, regulatory or other legal action, and fines

Weather Disruption8 filing receipts65% confidence46% max materialitymixed

Weather

Weather disruption

Weather Disruption58% confidence

events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political instability. Catastrophes can also cause losses in non-property business such as mortgage insurance, workers’ compensation or general liability. In addition to the nature of property business, we believe

into the risk management framework of our mortgage group to monitor and manage our exposure to potential (i) losses related to the direct physical impact of extreme weather conditions or events in certain transactions; and/or (ii) adverse economic or housing market conditions caused by the physical impact of extreme weather conditions or events on a region or the financial impact of transitioning to a zero or low carbon economy on a region. Generally, mortgage insurance policies exclude direct physical los

events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political instability. Catastrophes can also cause losses in non-property business such as mortgage insurance, workers’ compensation or general liability. In addition to the nature of property business, we believe

Natural catastrophes can be caused by various events, including hurricanes, floods, wildfires, tsunamis, windstorms, earthquakes, hailstorms, tornadoes, severe winter weather, fires, droughts and other natural disasters. The frequency and severity of natural catastrophe activity has also been greater in recent years due to climate change caused in part by human actions and other related factors. Catastrophes can cause losses in non-property business such as workers’ compensation or general liability. In ad

events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political instability. Catastrophes can also cause losses in non-property business such as mortgage insurance, workers’ compensation or general liability. In addition to the nature of property business, we believe

into the risk management framework of our mortgage group to monitor and manage our exposure to potential (i) losses related to the direct physical impact of extreme weather conditions or events in certain transactions; and/or (ii) adverse economic or housing market conditions caused by the physical impact of extreme weather conditions or events on a region or the financial impact of transitioning to a zero or low carbon economy on a region. Generally, mortgage insurance policies exclude direct physical los

Natural catastrophes can be caused by various events, including hurricanes, floods, wildfires, tsunamis, windstorms, earthquakes, hailstorms, tornadoes, severe winter weather, fires, droughts and other natural disasters. The frequency and severity of natural catastrophe activity has also been greater in recent years due to climate change caused in part by human actions and other related factors. Catastrophes can cause losses in non-property business such as workers’ compensation or general liability. In ad

events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political instability. Catastrophes can also cause losses in non-property business such as mortgage insurance, workers’ compensation or general liability. In addition to the nature of property business, we believe

Public Health6 filing receipts67% confidence46% max materialitymixed

Public HealthTariffs

Public health

Public Health65% confidence

TAL 53 2026 FIRST QUARTER FORM 10-Q Table of Contents CATASTROPHIC AND SEVERE ECONOMIC EVENTS We have large aggregate exposures to natural and man-made catastrophic events, pandemic events and severe economic events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political inst

is not incorporated by reference into this report. CATASTROPHIC AND SEVERE ECONOMIC EVENTS We have large aggregate exposures to natural and man-made catastrophic events, pandemic events and severe economic events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political inst

thereby increase the frequency of claims beyond our modeled results. Global recessionary conditions, including inflation, the slow recovery of certain sectors from the pandemic, predicted slow growth rates across key markets and other factors, will impact the insurance and reinsurance industry. While our business has not been directly impacted by the existing and proposed Trump administration tariffs on imported goods, there may be a ripple effect on how these impact certain industries where we provide insura

TAL 53 2026 FIRST QUARTER FORM 10-Q Table of Contents CATASTROPHIC AND SEVERE ECONOMIC EVENTS We have large aggregate exposures to natural and man-made catastrophic events, pandemic events and severe economic events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political inst

thereby increase the frequency of claims beyond our modeled results. Global recessionary conditions, including inflation, the slow recovery of certain sectors from the pandemic, predicted slow growth rates across key markets and other factors, will impact the insurance and reinsurance industry. While our business has not been directly impacted by the existing and proposed Trump administration tariffs on imported goods, there may be a ripple effect on how these impact certain industries where we provide insura

is not incorporated by reference into this report. CATASTROPHIC AND SEVERE ECONOMIC EVENTS We have large aggregate exposures to natural and man-made catastrophic events, pandemic events and severe economic events. Natural catastrophes can be caused by various events, including hurricanes, floods, windstorms, earthquakes, hailstorms, tornadoes, explosions, severe winter weather, fires, droughts and other natural disasters. Man-made catastrophic events may include acts of war, acts of terrorism and political inst

Labor Market4 filing receipts72% confidence46% max materialitynegative

LaborWages

Labor costs and availability

Labor Cost72% confidence

(collectively, “Barbican”). Our Ireland-based carrier, Arch Insurance (EU) Designated Activity Company (“Arch Insurance (EU)”) writes primarily European Union (“EU”) business with branches in Italy, Spain, France, the Netherlands and the U.K. On August 1, 2024 we expanded our U.S. middle market presence with the acquisition of Allianz’s U.S. Middle Market Property and Casualty insurance business and U.S. Entertainment business, representing an important part of our growth strategy in the

relevant to certain lines of business, the impact of which is difficult to accurately assess at this time. For example, in our mortgage business, the failure of general wages to keep pace with economic inflation, or increases in unemployment due to prolonged recessionary conditions, could prevent borrowers from being able to afford their mortgage payments and thereby increase the frequency of claims beyond our modeled results. Global recessionary conditions, including inflation, the slow recovery of certain se

(collectively, “Barbican”). Our Ireland-based carrier, Arch Insurance (EU) Designated Activity Company (“Arch Insurance (EU)”) writes primarily European Union (“EU”) business with branches in Italy, Spain, France, the Netherlands and the U.K. On August 1, 2024 we expanded our U.S. middle market presence with the acquisition of Allianz’s U.S. Middle Market Property and Casualty insurance business and U.S. Entertainment business, representing an important part of our growth strategy in the

relevant to certain lines of business, the impact of which is difficult to accurately assess at this time. For example, in our mortgage business, the failure of general wages to keep pace with economic inflation, or increases in unemployment due to prolonged recessionary conditions, could prevent borrowers from being able to afford their mortgage payments and thereby increase the frequency of claims beyond our modeled results. Global recessionary conditions, including inflation, the slow recovery of certain se

Healthcare Policy1 filing receipt75% confidence46% max materialitymixed

Drug PricingHealthcare Policy

Drug pricing and healthcare policy

Drug Pricing75% confidence

is awarded a cash bonus to recognize their accomplishments. We also encourage employees to continue their educational and professional development through tuition reimbursement plans. To attract the best talent to our industry, we offer internship programs and an Early Career Program with an Underwriting Track which provides participants with a robust introduction and real technical skills to build a successful career at Arch. Experienced professionals at Arch may participate in manager and leadership de

The Atlanta Fed's search for a new president has grown complicated. Finalists interviewed in April did not advance to the next stage in Washington, and some people familiar with the process say the search is rebooting.

The Dallas Fed's "trimmed mean" PCE was up 2.8% annualized in May, and those prices rose 2.4% over the previous 12 months. As noted before, this measure trims more from the top than the bottom An alternate measure from…

A motorist fills up the tank of a vehicle at a Conoco gasoline station Saturday, May 30, 2026, in Denver. (File photo: AP/David Zalubowski) WASHINGTON: The US Federal Reserve's preferred inflation measure hit a fresh th

Cruzeiro’s first half of 2026 was marked by heavy spending in the transfer market, totaling R$180.5 million on signings in the January window.However, the immediate on-field return fell short of exp...

CurrenciesJapanese currency near two-year low as rate gap pressures mountThe Bank of Japan raised its policy rate to 1% on Tuesday, but the move had been largely priced in, limiting support for the yen. (Photo by Akira…

The clock is ticking on Social Security’s main safety net — and for many in Mississippi, the impact could show up directly in their monthly checks.A trust fund could be fully dried out by the end of 2032. The latest…

Canadian UFC fans will no longer have to buy pay-per-views to watched numbered events, starting in 2027. This concept is nothing new to those in the United States, who have had numbered UFC events cooked into their…

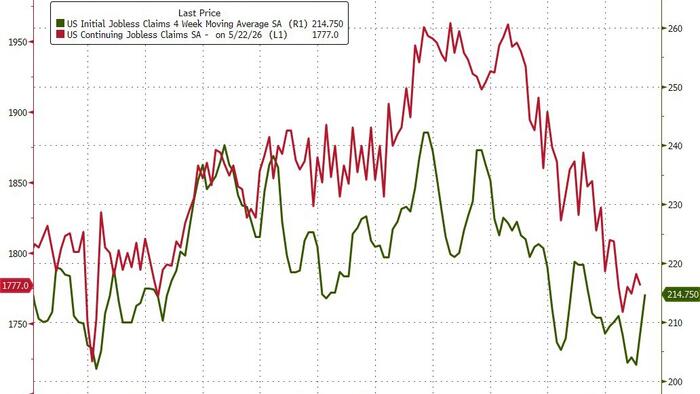

Jobless Claims Jump As US Tech Firms Announce Most Job Cuts In 2 Years The number of Americans filing for unemployment benefits for the first time jumped to its highest in three months last week at 225k (215k exp), but…

Social Security faces a looming depletion date for its retirement trust fund. A new report looks at how much benefit cuts Americans may see to their benefits.

Millions Of Americans Are Giving Up On Buying New Cars A growing number of Americans can no longer afford to buy new vehicles. Since 2020, roughly one million potential buyers have exited the market, and industry…

US natural gas futures declined as flows to liquefied natural gas export terminals dropped to the lowest since late January, leaving more supplies within the domestic market.

[The Conversation Africa] Robert Kyagulanyi Ssentamu, popularly known as Bobi Wine, is a Ugandan music star and political leader currently in exile. Framing his movement as a "people power" struggle by young Ugandans…