Interest expense and financing costs

Interest Expense89% confidenceincrease in our indebtedness or future borrowing costs

10-K · section 1AView source

$278.83

$0.3700 (-0.13%)

Last quote Jul 10, 7:59 PM

1D return

-0.13%

1W return

—

1M return

—

1Y return

—

ALL return

—

Price performance

—

AIZ's prediction-market exposure set spans Foreign exchange, Tariffs & trade policy, Interest rates, and Weather & catastrophe. Coverage: 3 filing-backed (SEC) and 2 broader macro/sector context.

Event exposure

3 documented filing links; 2 company, sector or macro context links. Relationship tier and confidence are shown on every row.

| Market | Relationship | Probability | Quote | Activity | State | Confidence |

|---|---|---|---|---|---|---|

| Documented exposure AIZ (Multi-line Insurance) discloses SEC-backed foreign exchange exposure: "during the fourth quarter of 2025 and the unfavorable impact of foreign exchange"; the impact can be mixed or context-dependent. Connection detailsduring the fourth quarter of 2025 and the unfavorable impact of foreign exchange Source receipt | 3% 97% NO 24H 2–3% | Bid 1¢ Ask 4¢ Spread 3.2 pts | $0.00 24H $687.4 total $203.28 liquidity | Open Closes Dec 31 | 83% accepted | |

| Documented exposure AIZ (Multi-line Insurance) discloses SEC-backed tariffs exposure: "markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and in"; the impact can be mixed or context-dependent. Connection detailsmarkets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition Source receipt | 1% 99% NO | Bid 1¢ Ask 1¢ Spread 0.1 pts | $2.0K 24H $826.9K total $428.1K OI | Open Closes Aug 1 | 82% accepted | |

Fed Rate Hike by April 2026 Meeting? polymarket · finance | Rates AIZ (Multi-line Insurance): included because this issuer's sector is structurally sensitive to rates, funding costs, credit, or capital allocation. Connection details | — | — Ask 0¢ Spread 0.1 pts | $42.4K 24H $87.2K total | Open Closes Dec 9 | 84% accepted |

| Hurricanes Weather AIZ (Multi-line Insurance): included because weather and hurricane outcomes can affect claims, power reliability, travel, facilities, or regional operations. Connection details | 4% 96% NO 24H 3–4% | Bid 3¢ Ask 4¢ Spread 1.0 pts | $1.6K 24H $2.7K total $2.6K OI | Open Closes Dec 1 | 80% accepted | |

| Documented exposure AIZ (Multi-line Insurance) discloses SEC-backed foreign exchange exposure: "during the fourth quarter of 2025 and the unfavorable impact of foreign exchange"; the impact can be mixed or context-dependent. Connection detailsduring the fourth quarter of 2025 and the unfavorable impact of foreign exchange Source receipt | 30% 70% NO | Bid 12¢ Ask 30¢ Spread 18.0 pts | $0.00 24H $30.4K total $7.2K OI | Open Closes Dec 31 | 83% accepted |

Operating risk graph

Kosmos extracts named operating factors from supported company filings. Expand a factor to inspect every returned receipt and its original source.

Factors

18

Mixed

89

Directional

11

increase in our indebtedness or future borrowing costs

including conditions in the financial markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

in the financial markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

(i) the impact of general economic, financial market and political conditions and conditions in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

• Catastrophe and non-catastrophe losses, including as a result of climate change and the current inflationary environment, could materially reduce our profitability and have a material adverse effect on our results of operations and financial condition

Adjusted EBITDA, our segment measure of profitability, as net income, excluding net realized gains (losses) on investments and fair value changes to equity securities, interest expense, benefit (provision) for income taxes, depreciation expense, amortization of purchased intangible assets, as well as other highly variable or unusual items (including restructuring costs, the loss on the pending subsidiary sale and non-core operations, each as described below). The following discussion covers the year ended Dec

Adjusted EBITDA, our segment measure of profitability, as net income, excluding net realized gains (losses) on investments and fair value changes to equity securities, interest expense, benefit (provision) for income taxes, depreciation expense, amortization of purchased intangible assets, as well as other highly variable or unusual items. 28 Executive Summary Summary of Financial Results Consolidated net income increased $127.5 million, or 87%, to $274.1 million for First Quarter 2026 from $146.6 million for

While interest rates and credit volatility are beginning to ease, inflation on parts and labor underscores the mixed macroeconomic environment

adversely affect our access to capital and our ability to pay our debts or expenses

(xx) a decrease in the value of our investment portfolio, including due to market, credit and liquidity risks, and changes in interest rates

(xx) a decrease in the value of our investment portfolio, including due to market, credit and liquidity risks, and changes in interest rates

While interest rates and credit volatility are beginning to ease, inflation on parts and labor underscores the mixed macroeconomic environment

adversely affect our access to capital and our ability to pay our debts or expenses

including conditions in the financial markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

objectives and targets, and our cash flows, results of operations and financial condition could be materially adversely affected. Each of our Global Lifestyle and Global Housing segments receives a substantial portion of its revenues from a few clients. A reduction in business with or the loss of one or more of our significant clients could have a material adverse effect on the results of operations and cash flows of individual segments or the Company. Reliance on a few significant clients may 20 weaken our bar

Connected Living”); and vehicle protection services, commercial equipment protection and other related services (referred to as “Global Automotive”); and • Global Housing: includes lender-placed homeowners, manufactured housing and flood insurance, as well as voluntary manufactured housing, condominium and homeowners insurance (referred to as “Homeowners”); and renters insurance and other products (referred to as “Renters and Other”). In addition, we report the Corporate and Other segment, which

provide exceptional customer experiences. We operate in North America, Latin America, Europe and Asia Pacific through two operating segments: Global Lifestyle and Global Housing. Through our Global Lifestyle segment, we provide mobile device solutions, extended service contracts and related services for consumer electronics and appliances, and credit and other insurance products (referred to as “Connected Living”); and vehicle protection services, commercial equipment protection and other related services (

Connected Living”); and vehicle protection services, commercial equipment protection and other related services (referred to as “Global Automotive”); and • Global Housing: includes lender-placed homeowners, manufactured housing and flood insurance, as well as voluntary manufactured housing, condominium and homeowners insurance (referred to as “Homeowners”); and renters insurance and other products (referred to as “Renters and Other”). In addition, we report the Corporate and Other segment, which

objectives and targets, and our cash flows, results of operations and financial condition could be materially adversely affected. Each of our Global Lifestyle and Global Housing segments receives a substantial portion of its revenues from a few clients. A reduction in business with or the loss of one or more of our significant clients could have a material adverse effect on the results of operations and cash flows of individual segments or the Company. Reliance on a few significant clients may 20 weaken our bar

Connected Living”); and vehicle protection services, commercial equipment protection and other related services (referred to as “Global Automotive”); and • Global Housing: includes lender-placed homeowners, manufactured housing and flood insurance, as well as voluntary manufactured housing, condominium and homeowners insurance (referred to as “Homeowners”); and renters insurance and other products (referred to as “Renters and Other”). In addition, we report the Corporate and Other segment, which

provide exceptional customer experiences. We operate in North America, Latin America, Europe and Asia Pacific through two operating segments: Global Lifestyle and Global Housing. Through our Global Lifestyle segment, we provide mobile device solutions, extended service contracts and related services for consumer electronics and appliances, and credit and other insurance products (referred to as “Connected Living”); and vehicle protection services, commercial equipment protection and other related services (

Connected Living”); and vehicle protection services, commercial equipment protection and other related services (referred to as “Global Automotive”); and • Global Housing: includes lender-placed homeowners, manufactured housing and flood insurance, as well as voluntary manufactured housing, condominium and homeowners insurance (referred to as “Homeowners”); and renters insurance and other products (referred to as “Renters and Other”). In addition, we report the Corporate and Other segment, which

economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

to drive innovation, contribute to the 4 development and adoption of sustainable products, and reduce the environmental impact of Assurant’s operations and supply chain

Our international operations face economic, political, legal, compliance, regulatory, operational, supply chain and other risks

to drive innovation, contribute to the 4 development and adoption of sustainable products, and reduce the environmental impact of Assurant’s operations and supply chain

Our international operations face economic, political, legal, compliance, regulatory, operational, supply chain and other risks

economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

financial market and political conditions and conditions in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

vehicle sales have shown modest improvements since 2024, remaining stable despite tariff uncertainty, while affordability challenges continue to steer more buyers toward the used vehicle market

For example, we face the risk of, the imposition of sanctions, tariffs, trade barriers or other protectionist laws or business practices that favor local competition (including from the United States), increase costs and may otherwise adversely affect our business

markets, the global economy, political conditions and the markets in which we operate, fluctuations in exchange rates, interest rates and inflation, and tariffs and global supply chain disruptions may have a material adverse effect on our results of operations or financial condition

For example, we face the risk of, the imposition of sanctions, tariffs, trade barriers or other protectionist laws or business practices that favor local competition (including from the United States), increase costs and may otherwise adversely affect our business

financial market and political conditions and conditions in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

vehicle sales have shown modest improvements since 2024, remaining stable despite tariff uncertainty, while affordability challenges continue to steer more buyers toward the used vehicle market

China and China-Taiwan trade tensions

(i) the impact of general economic, financial market and political conditions and conditions in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

China and China-Taiwan trade tensions

(i) the impact of general economic, financial market and political conditions and conditions in the markets in which we operate, including inflation, geopolitical conflict in the Middle East, tariff policies in the United States and abroad, global supply chain impacts and recessionary pressures

certain catastrophe-prone locations, such as Florida, California and Texas, may increase. The withdrawal of other insurers from these or other states may lead to adverse selection and increased use of our products in these areas, and it may negatively affect our loss experience and increase our costs. Negative publicity relating to our business, industry or clients may have a material adverse effect on our financial results. We communicate with and distribute our products and services ultimately to individual cu

methods to apply; • trends in loss frequency and severity for various causes of loss; • consideration of the distribution of loss reserves, management’s selection of the best estimate that may exceed an estimate based on median values, suggesting that favorable development may be more likely than unfavorable development; and • hindsight testing of prior loss estimates - the loss estimates on some product lines will vary from actual loss experience more than others. When employing the reserving

condition and results of operations. If we experience a business continuity event, such as an earthquake, hurricane, flood, terrorist incident, military conflict, pandemic, security breach, cybersecurity incident, power loss, telecommunications outage or other systems failure, or other disaster, our ability to continue operations will depend on an effective business continuity and disaster recovery plan, including the safety and continued availability of our personnel, including key executives, vendors a

condition and results of operations. If we experience a business continuity event, such as an earthquake, hurricane, flood, terrorist incident, military conflict, pandemic, security breach, cybersecurity incident, power loss, telecommunications outage or other systems failure, or other disaster, our ability to continue operations will depend on an effective business continuity and disaster recovery plan, including the safety and continued availability of our personnel, including key executives, vendors a

include insurance tracking, physical damage insurance and service contracts. Distribution and Clients Global Lifestyle operates globally, with approximately 80.7% of its revenue from North America (the U.S. and Canada), 7.7% from Latin America (Brazil, Argentina, Puerto Rico, Mexico, Chile, Colombia and Peru), 5.9% from Europe (the United Kingdom (the “U.K.”), France, Italy, Spain, Germany and the Netherlands) and 5.7% from Asia Pacific (Japan, Australia, New Zealand, South Korea, India, Singapore and Hong

devices, carrier promotional programs and sales prices for used devices, as well as to changes in consumer preferences and client forecasts and demands. Our Homeowners revenue is impacted by changes in the housing market, as well as the voluntary insurance market. Variability in insurance claims, including changes in frequency and severity, and the impact of inflation, also contribute to fluctuations in our business performance. In addition, across many of our businesses, we must respond to competitive pressu

material risks that could adversely affect our business, financial condition, results of operations and cash flows. 18 Business, Strategic and Operational Risks • Our revenues and profits may decline if we are unable to maintain relationships with significant clients, distributors and other parties, or renew contracts with them on favorable terms, or if those parties face financial, reputational or regulatory issues. • Significant competitive pressures, changes in customer preferences and disruption could

devices, carrier promotional programs and sales prices for used devices, as well as to changes in consumer preferences and client forecasts and demands. Our Homeowners revenue is impacted by changes in the housing market, as well as the voluntary insurance market. In addition, across many of our businesses, we must respond to competitive pressures, including the threat of disruption and competition for talent. For more information on these and other factors that could affect our results, see “Item 1A—Risk

devices, carrier promotional programs and sales prices for used devices, as well as to changes in consumer preferences and client forecasts and demands. Our Homeowners revenue is impacted by changes in the housing market, as well as the voluntary insurance market. Variability in insurance claims, including changes in frequency and severity, and the impact of inflation, also contribute to fluctuations in our business performance. In addition, across many of our businesses, we must respond to competitive pressu

material risks that could adversely affect our business, financial condition, results of operations and cash flows. 18 Business, Strategic and Operational Risks • Our revenues and profits may decline if we are unable to maintain relationships with significant clients, distributors and other parties, or renew contracts with them on favorable terms, or if those parties face financial, reputational or regulatory issues. • Significant competitive pressures, changes in customer preferences and disruption could

devices, carrier promotional programs and sales prices for used devices, as well as to changes in consumer preferences and client forecasts and demands. Our Homeowners revenue is impacted by changes in the housing market, as well as the voluntary insurance market. In addition, across many of our businesses, we must respond to competitive pressures, including the threat of disruption and competition for talent. For more information on these and other factors that could affect our results, see “Item 1A—Risk

include insurance tracking, physical damage insurance and service contracts. Distribution and Clients Global Lifestyle operates globally, with approximately 80.7% of its revenue from North America (the U.S. and Canada), 7.7% from Latin America (Brazil, Argentina, Puerto Rico, Mexico, Chile, Colombia and Peru), 5.9% from Europe (the United Kingdom (the “U.K.”), France, Italy, Spain, Germany and the Netherlands) and 5.7% from Asia Pacific (Japan, Australia, New Zealand, South Korea, India, Singapore and Hong

(xxviii) the costs of complying with, or the failure to comply with, extensive laws and regulations to which we are subject, including those related to privacy, data security, data protection and tax

Legal and Regulatory Risks • We are subject to extensive laws and regulations, which increase our costs and could restrict the conduct of our business, and violations or alleged violations of such laws and regulations could have a material adverse effect on our reputation, business and results of operations

Regulation We are subject to extensive federal, state and international regulation and supervision in the jurisdictions in which we do business

These dividend regulations vary by jurisdiction and by type of insurance provided by the applicable subsidiary, but generally require our insurance subsidiaries to maintain minimum solvency requirements and limit the amount of dividends they can pay to the holding company

Regulation We are subject to extensive federal, state and international regulation and supervision in the jurisdictions in which we do business

(xxviii) the costs of complying with, or the failure to comply with, extensive laws and regulations to which we are subject, including those related to privacy, data security, data protection and tax

Legal and Regulatory Risks • We are subject to extensive laws and regulations, which increase our costs and could restrict the conduct of our business, and violations or alleged violations of such laws and regulations could have a material adverse effect on our reputation, business and results of operations

These dividend regulations vary by jurisdiction and by type of insurance provided by the applicable subsidiary, but generally require our insurance subsidiaries to maintain minimum solvency requirements and limit the amount of dividends they can pay to the holding company

(xvi) fluctuations in exchange rates, including in the current environment

during the fourth quarter of 2025 and the unfavorable impact of foreign exchange

foreign tax and trade policies, the imposition of tariffs or other trade restrictions, other government actions and foreign currency fluctuations

(xvi) fluctuations in exchange rates, including in the current environment

during the fourth quarter of 2025 and the unfavorable impact of foreign exchange

foreign tax and trade policies, the imposition of tariffs or other trade restrictions, other government actions and foreign currency fluctuations

We leverage those insights to invest in emerging technologies and operations, including digital capabilities supported by artificial intelligence (“AI”), to introduce innovative products and services and continuously adapt those offerings to the changing needs of consumers

modify and maintain business practices to comply with U

We leverage those insights to invest in emerging technologies and operations, including digital capabilities supported by artificial intelligence (“AI”), to introduce innovative products and services and continuously adapt those offerings to the changing needs of consumers

(iii) significant competitive pressures, changes in customer preferences and disruption, including the impact of artificial intelligence

modify and maintain business practices to comply with U

the usefulness or desirability of the devices and parts, physical problems resulting from faulty design or manufacturing, increased competition, decreased consumer demand, including due to changes in customer preferences, changes in client promotions and seasonality, changes in client forecasts and demand, supply chain constraints and our ability to manage inventory, growing industry emphasis on cost containment

The evolving nature of consumer needs and preferences and improvements in technology could result in a reduction in consumer demand and in the prices of the products and services we offer

The evolving nature of consumer needs and preferences and improvements in technology could result in a reduction in consumer demand and in the prices of the products and services we offer

the usefulness or desirability of the devices and parts, physical problems resulting from faulty design or manufacturing, increased competition, decreased consumer demand, including due to changes in customer preferences, changes in client promotions and seasonality, changes in client forecasts and demand, supply chain constraints and our ability to manage inventory, growing industry emphasis on cost containment

breaches of our technology systems or those of third parties with whom we do business, or the failure to protect the security of data in such systems, including due to cyberattacks and as a result of working remotely; (xxviii) the costs of complying with, or the failure to comply with, extensive laws and regulations to which we are subject, including those related to privacy, data security, data protection and tax; (xxix) the impact of litigation and regulatory actions; (xxx) reductions or deferrals in the in

13 applicable to us, see “Item 1A – Risk Factors – Business, Strategic and Operational Risks,” “Item 1A – Risk Factors – Technology, Cybersecurity and Privacy Risks” and “Item 1A – Risk Factors – Legal and Regulatory Risks

Technology, Cybersecurity and Privacy Risks • The failure to effectively maintain and modernize our technology systems and infrastructure and integrate those of acquired businesses could adversely affect our business

and upgrade volumes, including based on the release of new devices and carrier promotional programs, as well as changes in client needs and customer preferences. U.S. new vehicle sales have shown modest improvements since 2024, remaining stable despite tariff uncertainty, while affordability challenges continue to steer more buyers toward the used vehicle market. Inventory of used vehicles has recovered slightly from the shortages of 2021-2022, but remains below historical levels, with scarcity of low-mileage ve

upfront fees, write-downs of deferred acquisition costs, insurance reserves held by third parties with or without collateral (including the impairment of any collateral), reimbursement of claims or commissions prepaid by us and loans granted to such counterparties. In addition, some of our agents, third-party administrators and clients collect and report premiums or pay claims on our behalf. Also, under certain contractual arrangements, we pay claims on behalf of third parties and subsequently seek reimbursement

In addition, inflationary pressures and shortages in the labor market have increased, and may continue to increase, our labor costs, including employee wages, and changes in interest rates has impacted, and may continue to impact, our investment portfolio and capital

with similar skill, scope and effort. We remain committed to remediate any significant pay disparities we may discover. We also continue to monitor and adjust market wages as necessary to ensure we provide competitive wages, consistent with our ongoing compensation strategy. We remain committed to investing in our people through competitive rewards and development opportunities. We continued to reward high performers and invest in merit increases, allocating more funding to front-line employees in recogniti

to execute our strategy, including through organic growth and the continuing service of key executives, senior leaders, highly-skilled personnel and a high-performing workforce; (v) the failure to find suitable acquisitions at attractive prices, integrate acquired businesses or divest of non-strategic businesses effectively; (vi) our inability to recover should we experience a business continuity event; (vii) the failure to manage vendors and other third parties on whom we rely to conduct business and provid

execution of our strategy, including through organic growth and the continuing service of key executives, senior leaders, highly-skilled personnel and a high-performing workforce.” For Twelve Months 2025, net cash provided by operating activities was $1.83 billion; net cash used in investing activities was $1.46 billion; and net cash used in financing activities was $364.2 million. We had $1.83 billion in cash and cash equivalents as of December 31, 2025. See “ – Liquidity and Capital Resources” below

to execute our strategy, including through organic growth and the continuing service of key executives, senior leaders, highly-skilled personnel and a high-performing workforce; (v) the failure to find suitable acquisitions at attractive prices, integrate acquired businesses or divest of non-strategic businesses effectively; (vi) our inability to recover should we experience a business continuity event; (vii) the failure to manage vendors and other third parties on whom we rely to conduct business and provid

execution of our strategy, including through organic growth and the continuing service of key executives, senior leaders, highly-skilled personnel and a high-performing workforce.” For Twelve Months 2025, net cash provided by operating activities was $1.83 billion; net cash used in investing activities was $1.46 billion; and net cash used in financing activities was $364.2 million. We had $1.83 billion in cash and cash equivalents as of December 31, 2025. See “ – Liquidity and Capital Resources” below

with similar skill, scope and effort. We remain committed to remediate any significant pay disparities we may discover. We also continue to monitor and adjust market wages as necessary to ensure we provide competitive wages, consistent with our ongoing compensation strategy. We remain committed to investing in our people through competitive rewards and development opportunities. We continued to reward high performers and invest in merit increases, allocating more funding to front-line employees in recogniti

In addition, inflationary pressures and shortages in the labor market have increased, and may continue to increase, our labor costs, including employee wages, and changes in interest rates has impacted, and may continue to impact, our investment portfolio and capital

First Quarter 2026 from $112.4 million for First Quarter 2025, mainly due to $132.3 million of lower pre-tax reportable catastrophes primarily related to the California wildfires. Excluding reportable catastrophes, Adjusted EBITDA decreased $8.0 million, or 3%, mainly driven by unfavorable non-catastrophe loss experience, including $7.6 million of lower favorable year-over-year non-catastrophe prior year reserve development. This decrease was partially offset by continued growth within Homeowners from higher l

businesses the Company has fully exited or expects to fully exit. Catastrophes include hurricanes, windstorms, tornados, earthquakes, hailstorms, floods, severe winter weather, wildfires, terrorist incidents and accidents, and may result in reportable catastrophe losses, which are individual catastrophe events that generate losses in excess of $5.0 million, pre-tax, net of reinsurance and client profit sharing adjustments, and including reinstatement and other premiums. Non-catastrophe losses include losses f

losses. Catastrophe events such as hurricanes typically occur in the second half of the year. We also experience some seasonal fluctuation in non-catastrophe weather-related claims that tend to occur in the first half of the year. Competition Our businesses focus on supporting, protecting and connecting major consumer purchases. Although we face global competition in each of our businesses, we believe that no single competitor competes against us in all of our business lines. 9 Across Global Lifesty

severity, which is a measure of the average size of claims. Factors affecting loss frequency include the effectiveness of loss controls, changes in economic activity and weather patterns. Factors affecting loss severity include changes in policy limits, retentions, rate of inflation and judicial interpretations. If the actual level of loss frequency and severity are higher or lower than expected, the ultimate reserves required will be different than management’s estimate. The effect of higher and lower levels

severity, which is a measure of the average size of claims. Factors affecting loss frequency include the effectiveness of loss controls, changes in economic activity and weather patterns. Factors affecting loss severity include changes in policy limits, retentions, rate of inflation and judicial interpretations. If the actual level of loss frequency and severity are higher or lower than expected, the ultimate reserves required will be different than management’s estimate. The effect of higher and lower levels

businesses the Company has fully exited or expects to fully exit. Catastrophes include hurricanes, windstorms, tornados, earthquakes, hailstorms, floods, severe winter weather, wildfires, terrorist incidents and accidents, and may result in reportable catastrophe losses, which are individual catastrophe events that generate losses in excess of $5.0 million, pre-tax, net of reinsurance and client profit sharing adjustments, and including reinstatement and other premiums. Non-catastrophe losses include losses f

losses. Catastrophe events such as hurricanes typically occur in the second half of the year. We also experience some seasonal fluctuation in non-catastrophe weather-related claims that tend to occur in the first half of the year. Competition Our businesses focus on supporting, protecting and connecting major consumer purchases. Although we face global competition in each of our businesses, we believe that no single competitor competes against us in all of our business lines. 9 Across Global Lifesty

First Quarter 2026 from $112.4 million for First Quarter 2025, mainly due to $132.3 million of lower pre-tax reportable catastrophes primarily related to the California wildfires. Excluding reportable catastrophes, Adjusted EBITDA decreased $8.0 million, or 3%, mainly driven by unfavorable non-catastrophe loss experience, including $7.6 million of lower favorable year-over-year non-catastrophe prior year reserve development. This decrease was partially offset by continued growth within Homeowners from higher l

loss at December 31, 2025 to a $170.1 million unrealized loss as of March 31, 2026, primarily due to an increase in Treasury rates. The following table shows the credit quality of our fixed maturity securities portfolio as of the dates indicated: Fair value as of Fixed Maturity Securities by Credit Quality March 31, 2026 December 31, 2025 Aaa / Aa / A $ 4,885.2 55.6 % $ 4,710.9 54.9 % Baa 3,266.0 37.2 % 3,257.9 38.0 % Ba 543.4 6.2 % 527.6 6.2 % B and lower 89.2 1.0 % 81.3 0.9 % Total $ 8,783.8 100.0 % $

loss at December 31, 2024 to a $55.7 million unrealized loss at December 31, 2025, primarily due to a reduction in U.S. Treasury rates. The following table shows the credit quality of our fixed maturity securities portfolio as of the dates indicated: Fair Value as of Fixed Maturity Securities by Credit Quality December 31, 2025 December 31, 2024 Aaa / Aa / A $ 4,710.9 54.9 % $ 3,987.5 55.6 % Baa 3,257.9 38.0 % 2,699.7 37.6 % Ba 527.6 6.2 % 415.7 5.8 % B and lower 81.3 0.9 % 72.2 1.0 % Total $ 8,577.7 100.0

Reported company facts

Latest comparable quarterly, annual or point-in-time values available from company XBRL filings.

Net margin

8.0%

Matching period Mar 31

Free cash flow proxy

$192.6M

Operating cash flow − capex · Mar 31

Revenue growth

+5.8%

Versus prior comparable quarterly

Net income growth

+3.2%

Versus prior comparable quarterly

Revenue

$3.42B

quarterly series · 8 periods

Values are reported company facts, not analyst estimates. Period comparability follows the available XBRL frames and may vary by issuer.

Disclosure timeline

Source documents are available as muted receipts; the derived context remains primary.

Related-market feed

These stories are attached to related prediction markets. They are context for the asset’s event exposures, not necessarily company-specific news.

The Atlanta Fed's search for a new president has grown complicated. Finalists interviewed in April did not advance to the next stage in Washington, and some people familiar with the process say the search is rebooting.

The Dallas Fed's "trimmed mean" PCE was up 2.8% annualized in May, and those prices rose 2.4% over the previous 12 months. As noted before, this measure trims more from the top than the bottom An alternate measure from…

A motorist fills up the tank of a vehicle at a Conoco gasoline station Saturday, May 30, 2026, in Denver. (File photo: AP/David Zalubowski) WASHINGTON: The US Federal Reserve's preferred inflation measure hit a fresh th

Gold Falls as Dollar Holds Firm on Fed Rate-Hike Expectations Discovery Alert

Fed June 2026 Meeting: Rate Hikes Back on Table as Dot Plot Shifts Hawkish Intellectia AI

CurrenciesJapanese currency near two-year low as rate gap pressures mountThe Bank of Japan raised its policy rate to 1% on Tuesday, but the move had been largely priced in, limiting support for the yen. (Photo by Akira…

Today, we look back at one of the few three-time All-Americans in Trojans history

The clock is ticking on Social Security’s main safety net — and for many in Mississippi, the impact could show up directly in their monthly checks.A trust fund could be fully dried out by the end of 2032. The latest…

Boxxer have made a deal with DAZN, starting with a rematch between Troy Williamson and Callum Simpson

The rookie cornerback is making a great first impression

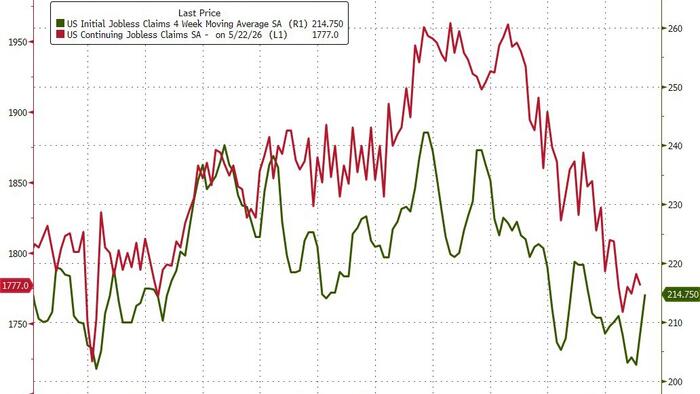

Jobless Claims Jump As US Tech Firms Announce Most Job Cuts In 2 Years The number of Americans filing for unemployment benefits for the first time jumped to its highest in three months last week at 225k (215k exp), but…

Social Security faces a looming depletion date for its retirement trust fund. A new report looks at how much benefit cuts Americans may see to their benefits.

Millions Of Americans Are Giving Up On Buying New Cars A growing number of Americans can no longer afford to buy new vehicles. Since 2020, roughly one million potential buyers have exited the market, and industry…

Even as Americans confront higher costs, millions of people have lost Supplemental Nutrition Assistance Program food benefits.

Price history: Kosmos reference feeds. Company facts and filing receipts: SEC EDGAR. Prediction-market relationships: Kosmos issuer graph. Related-market context may include broader sector or macro coverage.